Maintaining physical inventories can be expensive and time-consuming. Thus, you need a periodic inventory system to track your inventory management. Let’s learn more about the various aspects of a periodic inventory.

Compare Top Inventory Management Software Leaders

What This Article Covers

- What Is a Periodic Inventory System?

- How Does It Work?

- Valuation Methods

- Advantages & Disadvantages

- Perpetual Inventory

- Who Should Use This Method?

- Conclusion

What Is a Periodic Inventory System?

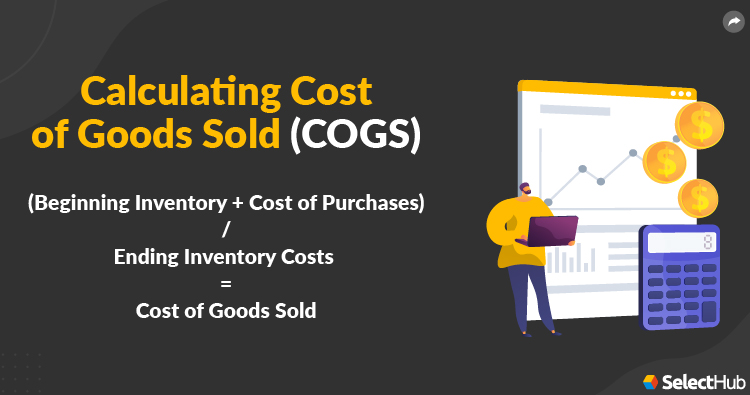

A periodic inventory system is an inventory management valuation method to determine the cost of goods sold (COGS) for accounting and financial reporting purposes. As its name implies, this solution requires physically taking inventory levels at designated periods.

Intervals between periods could be as short as a week or a month. However, because physically counting inventory generally takes an excessive amount of time and staffing, especially for larger product quantities, many companies set quarterly or annual accounting periods.

Since inventory counts happen at the end of an accounting period, you must rely on estimates to understand COGS during intervals. When ending inventory is determined, you use it to adjust estimates to reflect actual counts.

Now you have an idea of what a periodic inventory system is. Let’s take a closer look at how this system works, some of its benefits and drawbacks, the alternative perpetual inventory system and who typically finds it most useful.

How Does It Work?

Periodic inventory systems don’t continuously update inventory accounts to reflect individual sales. Instead, you manually edit these values at the end of your specified time interval. Because of this, the method requires keeping personal accounts for beginning inventory, purchases and on-hand inventory.

This valuation method is quite simple to execute. You take the beginning inventory costs for a period, add the cost of inventory purchases during the interval and subtract the cost of your remaining inventory after you’ve gathered your ending count. The result is your cost of goods sold.

In addition to accounts for beginning inventory, purchases and ending inventory, you’ll want to keep track of sales. It won’t directly impact your inventory account since the numbers aren’t adjusted until you have your ending counts. That said, you can compare recorded sales to beginning and ending counts at the end of a period to ensure products aren’t missing.

Now that we’ve established the basic process of a periodic inventory system, we can check out some of the individual methods used under these solutions.

Valuation Methods

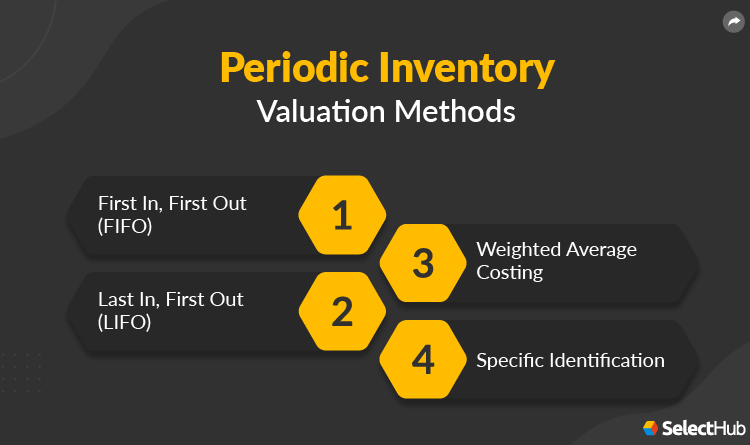

There are three standard inventory valuation methods for a periodic inventory system and a fourth less common approach. These main methods include first-in, first-out (FIFO), last-in, last-out (LIFO) and weighted average costing. There’s also the less widely used specific identification.

Let’s break down each method:

- FIFO: With the first-in, first-out method, you sell your products in order from oldest to newest. This means you’ll take stock of the most recently purchased items at the end of your accounting period. In addition, costs are assigned based on the most recent price of purchased goods.

- LIFO: Last-in, first-out is similar to FIFO in that it requires selling goods in a particular order. However, instead of selling the oldest items first, you sell the most recently purchased items. At the end of your accounting period, you’re left with the oldest stock, and the cost of goods sold will reflect the price of these purchases rather than the most recent prices.

- Weighted Average Costing: Rather than valuing stock based on the newest or oldest price of purchased goods, weighted average costing takes both into account and lands you somewhere in between. To determine your weighted average, you take the cost of your beginning inventory, add the cost of purchases made during the period and divide by the number of available items for sale.

- Specific Identification: Finally, you can use specific identification. If you choose this method, prepare to keep in-depth records relating to inventory quantities and costs for individual items. It requires you to document each item’s individual cost, including additional costs relating to the item prior to selling it, instead of grouping purchases together.

Advantages and Disadvantages

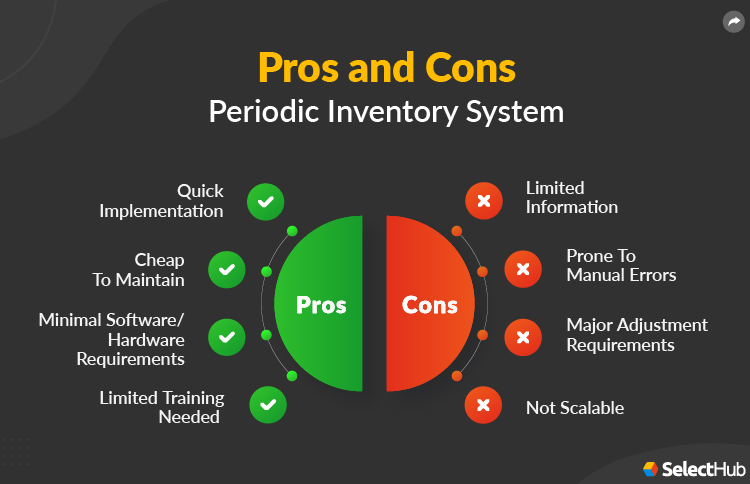

Deploying a periodic inventory system can prove advantageous, especially for smaller companies. It’s undoubtedly cheaper to implement and maintain than a perpetual inventory system, and because of its simplicity, it doesn’t require extensive employee training.

Let’s take a look at some of its advantages and disadvantages:

Advantages

Here are some of the benefits you can expect from using the periodic inventory method:

- Cheap Implementation: In its simplest form, periodic inventory doesn’t require anything more than a pen and paper. You can record data and make changes or updates by hand. However, basic software solutions, such as Microsoft Excel, help simplify the process and keep a digital trail for inventory counts. Either way, you won’t have to plan for high upfront costs to begin using a periodic inventory system.

- Limited Training: Physically counting inventory can be a time-consuming process, but it’s not a complicated one. It requires employees to tally up remaining stock numbers at the end of your accounting period. You may need to allocate additional funds for staffing purposes when inventory days roll around, but you won’t need to train staff to use complicated solutions to record and track sales constantly. This factor is especially beneficial for companies and industries with high turnover rates.

No solution is perfect, though, and periodic inventory isn’t an exception. While it’s simple and cost-effective, it does come with its own set of drawbacks.

Disadvantages

Now, let’s take a look at some of the pitfalls associated with periodic inventory systems:

- Limited Information: Information is only collected and updated at the end of an accounting period. Because of this, you can’t see COGS and inventory balances during these periods. Instead, you’ll have to rely on estimates for an idea of financial standings, which presents its own problems.

- Error-prone: Although estimating COGS can be a viable solution for small-scale businesses, it’s not likely worth the headache for any company dealing with medium to large amounts of inventory. Estimations, no matter how thorough, will require quite a few adjustments once you actually take stock of your ending inventory for a particular period.

- Adjustment Requirements: When you’ve determined your remaining inventory at the end of the accounting period, you’ll likely be left with some severe adjustment requirements to match your estimates to actual numbers. More extensive quantity inventories will require significantly more adjusting than smaller ones.

- Doesn’t Scale: Even if your business is on the smaller end now, it may be worth looking into alternative inventory management solutions if you want to expand at any point in the future. As your on-hand inventory grows, so too will the amount of time and effort needed to physically count products, estimate the cost of goods sold and adjust estimates to reflect actual counts.

Perpetual Inventory

We touched on perpetual inventory above, but let’s take a closer look before we start wrapping things up.

Perpetual inventory systems, as the name suggests, continuously update inventory accounts to adjust for individual sales. You typically use some form of supply chain management software coupled with digital input devices, including point-of-sale systems and barcode scanners or RFID readers, to facilitate inventory tracking.

Perpetual inventory systems use the same methods as a periodic system: FIFO, LIFO, WAC and specific identification. The methods themselves are basically used the same way they are in a periodic inventory system; however, there is one crucial difference.

Instead of using these methods to calculate one COGS amount at the end of an accounting period, the perpetual system calculates COGS (you guessed it) perpetually. The cost of goods sold is determined after every transaction.

Due to their software and peripheral requirements, implementing a perpetual method comes with higher overhead costs than periodic inventory systems. However, they significantly reduce the amount of time, payroll costs and hassle you’ll face if you have a sizable on-hand inventory. Eating the upfront costs of a perpetual system can result in money-saved down the line.

Who Should Use This Method?

Given the information we’ve covered up to this point, it’s clear that periodic systems are best suited to small businesses or companies that provide high-end products with a low on-hand inventory. Moreover, they’re an excellent option for companies that aren’t looking to expand their inventory in the future.

Turnover rate is another consideration you’ll want to address. If you’re regularly cycling through employees, a periodic system can help you minimize training time and costs. You can quickly train your employees on your preferred method of taking physical inventory counts rather than regularly training new hires to use complex software and hardware.

Finally, your available capital for upfront costs may sway your decision one way or another. If you’re planning to grow your business and need a solution that will scale, we don’t recommend a periodic system.

In this case, investing in a perpetual inventory system right out of the gate could save you money in the long run, not to mention some intense headaches. But if you’re only looking to offer products to your local community, an Excel spreadsheet, diligent counting and a periodic inventory method may be all you need!

Conclusion

Determining the proper inventory accounting method for your business is a crucial step to financial success. At the end of the day, you’ll have to decide what will work best for your needs.

Suppose you’re running a mom-and-pop shop with a reasonably small inventory. In that case, a periodic inventory system could be enough to meet your needs without breaking the bank on software and hardware purchases. If that’s not the case, you may need to consider alternative options.

How have you successfully implemented an inventory management strategy? Let us know your thoughts on periodic inventory systems in the comments below.