The financial industry is updating its business practices to enhance productivity and remain relevant among its competitors and clientele. One upgrade the accounting industry is implementing is automation. In short, accounting automation refers to the process of automating financial processes and streamlining tasks such as bookkeeping, data entry and analyzing crucial documents, usually by leveraging the powers of artificial intelligence (AI) and implementing accounting software.

Compare Top Accounting Software Leaders

By 2024, experts believe artificial intelligence in this field will gain $4.7 million at a compound annual growth rate (CAGR) of 48.4%. Automated accounting can help free up professional accountants’ time to provide genuine counsel to their clients and handle jobs that require critical thinking and judgment – something AI can’t do.

Let’s examine the overview of accounting automation, its features and other branches of AI.

What This Article Covers

What is Accounting Automation?

As aforementioned, accounting automation employs AI to automate repetitive tasks such as bank reconciliations, paying bills, payroll, general ledger and more.

History

Accountants and bankers began discussions on utilizing automation to improve their efficiency in the 1950s. However, the idea dates back to the mid-18th century.

Bayesian Statistics

Thomas Bayes, an English theologian and mathematician, established a new means of statistics in his 1763 paper, “Essay Towards Solving a Problem in the Doctrine of Chances.” It answers this question: If a pattern frequently occurs in previous data trials, how do you know the same pattern will continue in the future? Bayes crafted a form of statistics that could assist in predicting recurring patterns in various sets of data. These statistics are a foundational cornerstone of accounting and are known today as Bayesian statistics.

In the 1960s, Robert Schlaifer, a managerial economics expert, made Bayesian Statistics famous. Schlaifer played with Bayesian Statistics to determine its effectiveness in making informed business decisions. Schlaifer’s book, “Probability and Statistics for Business Decision,” led to more people conducting research and evaluating how statistics can impact the business world and auditors.

Expert Systems

AI in finance launched officially in the 1980s with the use of multiple expert systems or knowledge-based systems. One notable expert system used in finance was Protrader, designed by two college professors, K.C. Chen from California State University and Ting-peng Liang from the University of Illinois at Urbana. Protrade’s objectives included:

- Monitoring premiums in the market

- Detecting elite optimum investment strategies

- Completing transactions when necessary and

- Altering the knowledge base through a learning mechanism

Another notable expert system was released In 1987 by Chase Lincoln First Bank and Arthur D. Little Inc. They unveiled the Personal Financial Planning System (PFPS) expert system. Its features included:

- Investment planning

- Debt planning

- Retirement planning

- Education planning

- Life-insurance planning

- Budget recommendations

- Income-tax planning

- Savings attainment for more major financial goals

The possibility of financial fraud detection gained popularity in the 1990s. The U.S. Department of Treasury employed the FinCEN Artificial Intelligence system (FAIS) in 1993 to pinpoint occurrences of money laundering. Since transactions required handwriting, FAIS rapidly analyzed handwriting to find discrepancies. In two years, FAIS spotted 400 potential money laundering cases that equated to $1 billion.

Although expert systems were the first grand step in accounting automation, they became extinct for two reasons: they either failed to meet clients’ expectations or were too complex to operate. Modern solutions aim to eliminate both of these problems and hopefully will be around for the long-haul.

Are Accountants’ Jobs at Risk?

With all this talk about software, some accountants are shaking in their boots, fearing that automation will take their jobs. They have a right to feel worried. A study says 29% of the accounting industry leverages automated technology.

However, if the manufacturing industry can adopt robots and create more opportunities, so can accounting. Sure, those that manage general ledgers, perform bank reconciliations, input account payables and receivables and other repetitive tasks will be at risk because automation can perform these tasks more swiftly and accurately. Up-and-coming accountants must consider diving into more prominent roles such as monetary planning, business management and financial gurus that businesses seek for advice.

After all, robots aren’t capable of thorough scrutiny, sound advice or tactical perceptions like the human mind. Accountants need to broaden their horizons and adapt, or they will become obsolete.

Since we’ve covered the definition, history and future of automated accounting, it’s time we review its perks.

Key Benefits

Mineral Tree stated that in 2020, companies who automated their accounts payable process saw electronic payment usage hit 21% instead of 16% for companies who have not used automation.

Read on for more perks that automation and AI provide in the bookkeeping sector.

Get our Accounting Software Requirements Template

1. Leverages Paperless Audits

Performing audits can be cumbersome and time-consuming. Yet, AI can simplify the process. Its digitization feature can automatically track which essential documents – such as audit plans, checklists, confirmation letters and more – were accessed by whom and when. The digitization feature can also boost the security of critical data and files. Thanks to digital file-sharing, you won’t need to spend countless hours hunting for documents in cluttered filing cabinets.

2. Reinforces Company Policies

AI ensures that you won’t have to worry about being unaware of employees abusing your corporate spending policies. AI can scan and review travel bookings, employee receipts, credit card transactions and more to monitor employee spendings. It can recognize expense violations, including unverifiable receipts, personal credit card usage and travel add-ons. It can also help you determine which policies are effective or ineffective.

3. Minimizes Fraud

A PwC study says 24% of companies have encountered fraud in the past two years. However, AI can pick up on patterns and pinpoint various ranges of inconsistencies in your financial data. When your data expands and circulates across multiple payment channels, your chances of fraud and discrepancies swiftly increase. Typically, auditors only examine non-compliant expense reports, which is a small percentage. On the other hand, AI can review and audit all of your spending reports, leaving no stones unturned. Lastly, since AI is adjustable, it can assess new financial information floods with the same degree of efficiency as it does when working with regular amounts of data.

Get our Accounting Software Requirements Template

4. Saves Time and Money

Letting automation manage mundane tasks enables you to focus your time and energy on more important business matters such as financial consultation, decision making, patron interaction and more.

Also, investing in automatic accounting software can help you save money on hiring an entire financial or payroll department because it can handle repetitive tasks. This move will allow you to handpick and mold accountants into financial advisors, partners or other critical roles to ensure a rewarding, unpredictable employment experience.

5. Dwindles Human Errors

Automation increases accuracy and depletes mistakes caused by human error. Let’s face it: humans aren’t perfect, especially with bookkeeping. Sometimes we make mistakes and don’t even notice it until the very last minute or when someone else points it out to us. AI typically looks for and corrects flaws rapidly during or after inputting information. Accounting does rely on accurate information such as totals, sales tax, discounts, payroll deductions and more, so AI would provide a great helping hand.

6. Protects Crucial Data

This digital age allows industries and companies to implement technology to its fullest extent. Accounting is no exception. It uses software, automation, the cloud and more to streamline production and even store various files in a secure space. This machinery reduces paper and saves office space by arranging documents in a digital environment and becomes accessible from virtually any location on any device with a reliable internet connection.

Imagine if, for example, you have a business meeting with a client halfway around the world and you accidentally lose or forget the required documents or records? Technology can alleviate these and other mishaps. You can even permit patrons to sign documents with a secure eSignature module.

These are just a handful of the benefits that come with adopting bookkeeping automation.

7. Extended Branches of AI

AI, like the many branches of a tree, has various subsets with unique features. These subsets make up the core of accounting automation. Let’s see how they can increase your firm’s productivity and put accountants in the driver’s seat of more meaningful work.

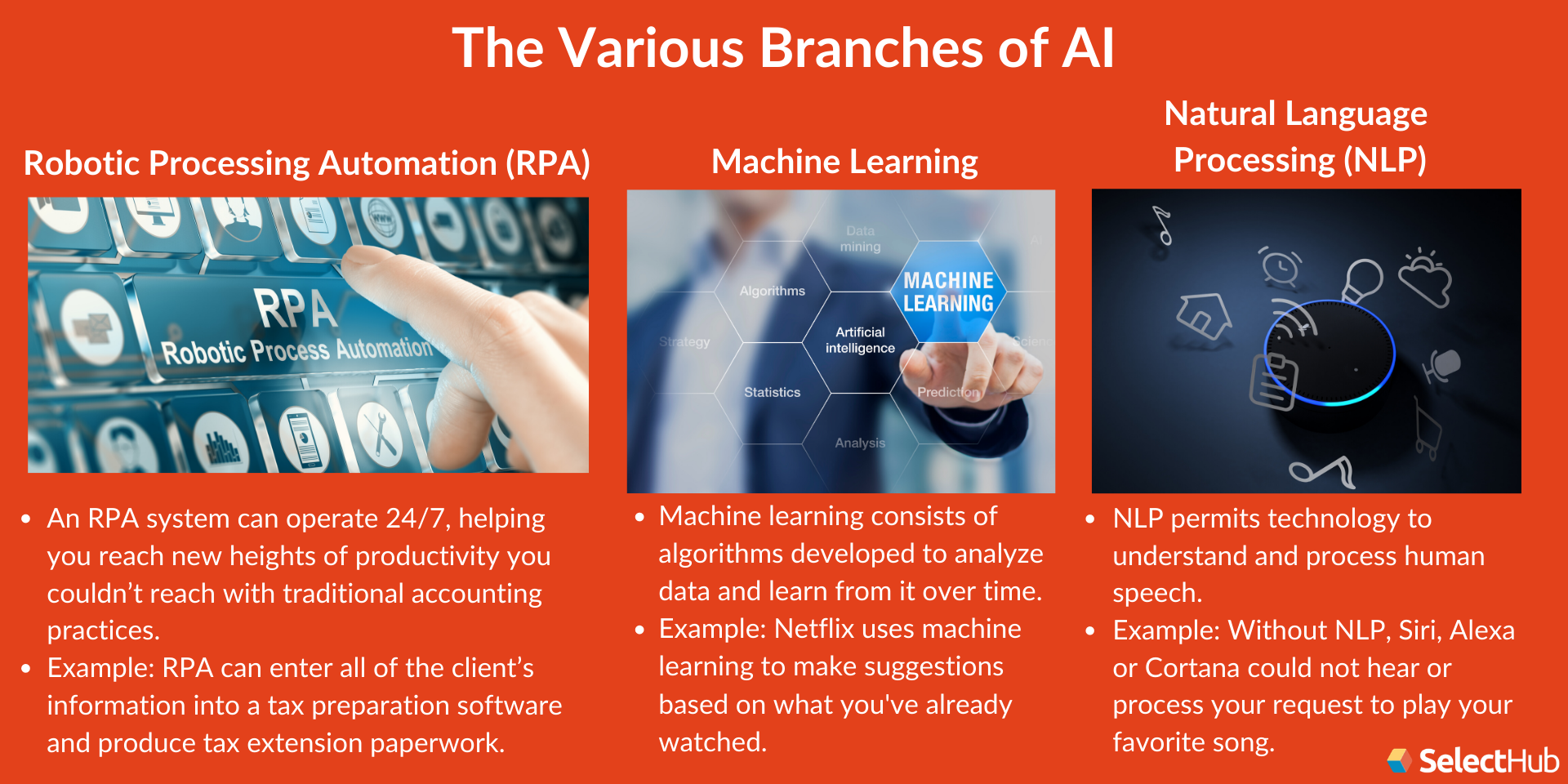

Machine Learning

One subset of AI is machine learning. In a nutshell, machine learning consists of algorithms developed to analyze data and learn from it over time. For example, Netflix uses machine learning. If you watch many comedy films, music documentaries and cooking shows, Netflix will find and recommend more of these genres for you. Machine learning can streamline accounting firms by simplifying bank reconciliations, perusing all of your audit data, clarifying invoice payments and generating cohesive risk assessments.

Handle Bank Reconciliations Hassle-Free

Machine learning can simplify bank reconciliations. After observing previous account choices and allocations, it can offer proper recommendations for new bank transactions. Implementing machine learning can also help in reducing errors and duplicate entries.

Review All Audit Data

Typically, auditors only review snippets of data for an audit. However, machine learning can perform multiple analyses on entire ledgers if necessary. After analyzing all of your data, it can give you lists of exceptions found to evaluate and ensure they’re all chronicled. As machine learning observes the conclusions an auditor makes when confirming or invalidating exceptions, it will pinpoint additional data points about the confirmations and invalidations and apply them to any extra exceptions it digs up. Lastly, machine learning can read receipts in foreign languages and guarantee they’re genuine and align with policies.

Absolve Invoice Payments

It’s a struggle for accounts receivable or treasury bookkeepers to clear invoice payments when customers either combine invoices into one payment, pay incorrect amounts or forget to include the invoice numbers on charges. The bookkeeper must add up various invoices that could or could not match the payment longhand or reach out to the customer to clarify payment information.

Machine learning can relieve some of these headaches. It can automatically suggest invoices that may match the paid amount, instantaneously clear short payments and immediately generate a delta invoice.

Chart Accurate Risk Assessments

There are plenty of customer variables for finance teams to consider when creating risk assessments, including maturity, size, current system landscape and more. Experienced managers usually tackle these projects. Although this strategy works to a certain degree, the decisions made for risk assessments are narrow because of narrow perspectives. Machine learning can broaden the horizon a bit.

Machine Learning will give teams access to every single implementation project ever created by the company. With all of this diverse information, they can chart new projects against previous projects and draft a well-informed risk assessment. The benefits include:

- Financial managers supplying customers with better offers using lower risk uplift.

- Guarantees the cover is enough in case the risk is high.

- Strengthens your company’s revenue and margin.

Get our Accounting Software Requirements Template

Natural Language Processing

Another subset of AI, natural language processing (NLP), permits technology to understand and process human speech. Without NLP, Siri, Alexa or Cortana could not hear or process your request to play your favorite song, recommend a movie or set a reminder for that prominent doctor’s appointment. NLP can maximize bookkeeping techniques by picking up varying tones of speech, exposing fraudulent behavior and more.

Read Positive or Negative Tones

If NLP analyzes large quantities of news articles, social media, reports and other web content, it can pinpoint positive or negative speech tones. Leveraging NLP’s analytical capabilities is vital because it can identify the true feelings shared in financial reports, between a client and a specific firm or between an investor and particular markets.

Detect and Expose Fraud

Along with other analytical techniques, NLP can assist in predicting and recognizing fraud activity. Usually, deceptive statements have obvious language tendencies, like an ample amount of negative-sentiment words and a diminished amount of first-person pronouns. NLP can surveil and expose these tendencies in emails, annual filings with the U.S. Securities and Exchange Commission (SEC), transcripts of conference calls and other corporate communication forms.

Natural Language Generation and Audits

Natural language generation (NLG), a subgroup of NLP, is a computer capability that can generate text into comprehensible human languages. NLG can help audits because it can analyze structured data and information used in charts and graphs and transform it into text for auditors to clarify.

An example of NLG is IBM OpenPages coinciding with IBM’s Watson. The internal audit management tool contains various risk domains, including IT governance, policy and compliance and operational risk management programs. Some of its key features include:

- Audit Planning: Creates work papers for audit execution.

- Organizes Work Papers: Hosts a unified library of electronic work papers and also automatically reviews and approves work papers.

- Monitors Resources: Monitors and supervises audit performances while tracking useful resources.

- Scheduling: Assists in creating multi-year audit plans

An example of AI accounting software.

Natural Language Understanding

Another branch of NLP is Natural Language Understanding (NLU). It can understand slang, mispronunciations, misspellings and other distinct qualities of human speech. NLU can also extract an immense amount of information, cipher out insignificant data and supply valuable content. Imagine having NLU sifting through thousands of checks, invoices, and receipts so you can focus your attention on tasks that require critical thinking and judgment.

Robotic Process Automation

Robotic process automation (RPA), another AI branch, can emulate repeatable tasks such as copying and pasting information the same way humans can. Its assorted features make it a key asset for even the most complex of bookkeeping dutie:

Effortlessly Input Tax Info

Tax preparers obtain numerous tax files and documents, from reporting forms to receipts and invoices. A majority of them come in as PDFs. Preparers spend loads of time inputting that information into spreadsheets and third-party tax preparation software. RPA can enter all of the client’s information into the tax preparation software and even produce tax extension paperwork.

Precise Analysis and Calculations

Peering over documents and forms collected in an audit is a full-time job. An RPA system can log into a client’s secure file transfer protocol (FTP) and obtain listings for current and prior year sales, trial balances and other audit-related evidence. This system can perform accurate calculations of the total sales per listing and correlate it to the total per trial balance. It can also gauge whether the total revenue amount from the current and prior year listings is different and create an alert if the difference surpasses the materiality threshold.

Uninterrupted 24/7 Operation

Do you need to pull an all-nighter to get those bank reconciliations completed? An RPA system can operate 24/7, helping you reach new heights of productivity you couldn’t achieve with traditional accounting practices. No supervision is necessary.

Compare Top Accounting Software Leaders

Moving Forward

Accounting automation and other types of accounting software are metamorphosing the finance industry. No matter what form of automation you invest in, be sure to pick one that aligns with your needs and preferences so you can boost your productivity and satisfy your clientele.

How has automation improved your accounting practices? Let us know in the comments!